I am particularly pleased to be here today for multiple reasons. I think most of us feel some nostalgic pull to these meetings, though I do not think I want to revisit the frantic interview cycle ever again. These meetings allow us to meet and reconnect with colleagues, hear about new and valuable research, and have in-depth discussions on the subtler, more nuanced aspects of economics. I hope to do that today with my co-panelists on a subject that has my and the Federal Open Market Committee's full attention: inflation. I want to use my time to outline the unique set of challenges facing policymakers and academics today as well as how we can better understand inflation dynamics in this new environment, including by looking at novel data sources.1

The effects of the pandemic and Russia's war against Ukraine have turned a spotlight on the supply side of the economy and its ability to adapt to rapid changes in demand and to navigate a seemingly never-ending sequence of adverse supply shocks. The unique nature of the supply and demand imbalances over the past couple of years has made it more difficult to forecast inflation, posing new challenges for monetary policy. One way to better manage these challenges is by continuing to monitor—and even expand—new sources of data. Additionally, we have some key issues to consider in approaching revised models of inflation behavior.

Before I turn to broader issues with modeling inflation, let me start with the recent inflation data. Inflation remains far too high, despite some encouraging signs lately, and is therefore of great concern. As a Fed policymaker, I am committed to bringing inflation back to our 2 percent goal.

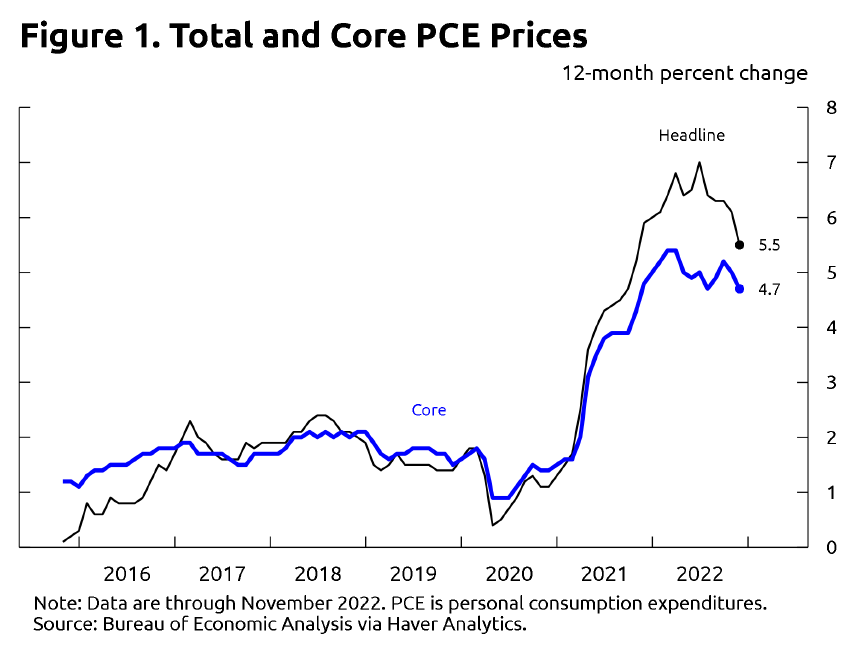

The 12-month change in total personal consumption expenditures (PCE) prices through November was 5.5 percent. Core PCE prices rose 4.7 percent over the same 12-month period (figure 1). This measure omits volatile food and energy prices and tends to give a more accurate signal of total inflation's trajectory. Both figures are down a bit from the peaks reached in the first half of last year. However, monthly data are quite volatile, so I would caution against putting too much weight on the past few favorable monthly data reports.

{kind=link}

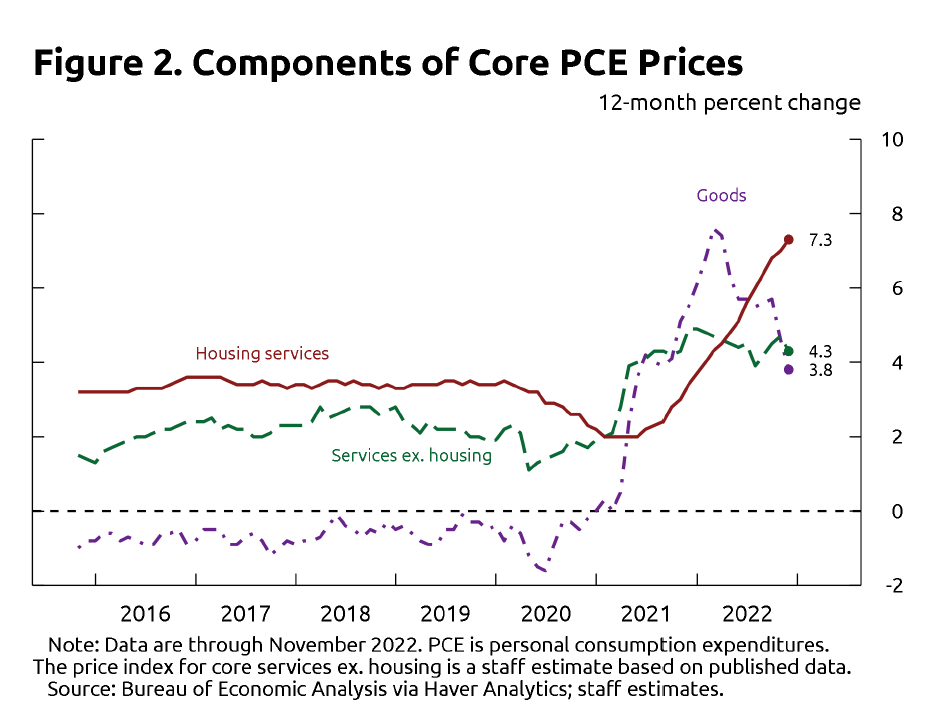

The high and volatile inflation seen over the past two years appears to reflect rapid shifts in demand, coupled with supply-chain disruptions. This has led to sizable demand–supply imbalances across different sectors. To analyze these influences, I find it useful to consider core inflation in three categories corresponding to distinct components of consumer spending: core goods inflation, housing services inflation, and inflation in core services other than housing (figure 2). In contrast to core goods inflation, which has declined over the past year, housing services inflation has continued to rise rapidly, and inflation in other core services has been little changed on balance. In the current environment, I find it helpful to examine a number of somewhat new indicators when assessing inflation pressures within each category.

{kind=link}

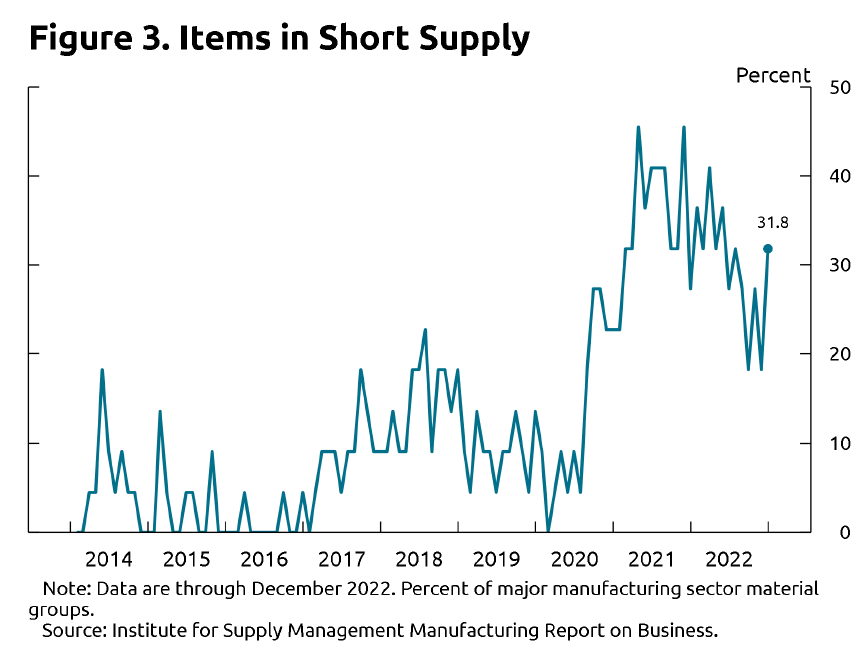

Starting with goods inflation, I have been closely observing indicators of capacity constraints along global and domestic supply chains. Shortages, bottlenecks, and other logistical issues have hampered production and boosted distribution costs for a significantly longer period than we had anticipated a couple of years ago. Fortunately, many indicators suggest that shortages of inputs have abated, and transportation costs have started to fall. For example, the list of industrial inputs that respondents to the Institute for Supply Management's (ISM) manufacturing survey indicate are in short supply is now shorter than it was at its peak at the end of 2021 (figure 3). Supply constraints are far from fully resolved, however, and respondents to the December ISM survey still reported difficulty procuring items such as electrical and hydraulic components, rubber and steel products, and—of course—semiconductors. The supply of semiconductors has been a particularly strong driver of inflation in the motor vehicle sector and has affected that sector's ability to produce vehicles—a matter I highlighted in a speech in Detroit in late November.

{kind=link}

Categories

Recent posts

Bank of Canada announces finalists for ...

10 Jan 2023